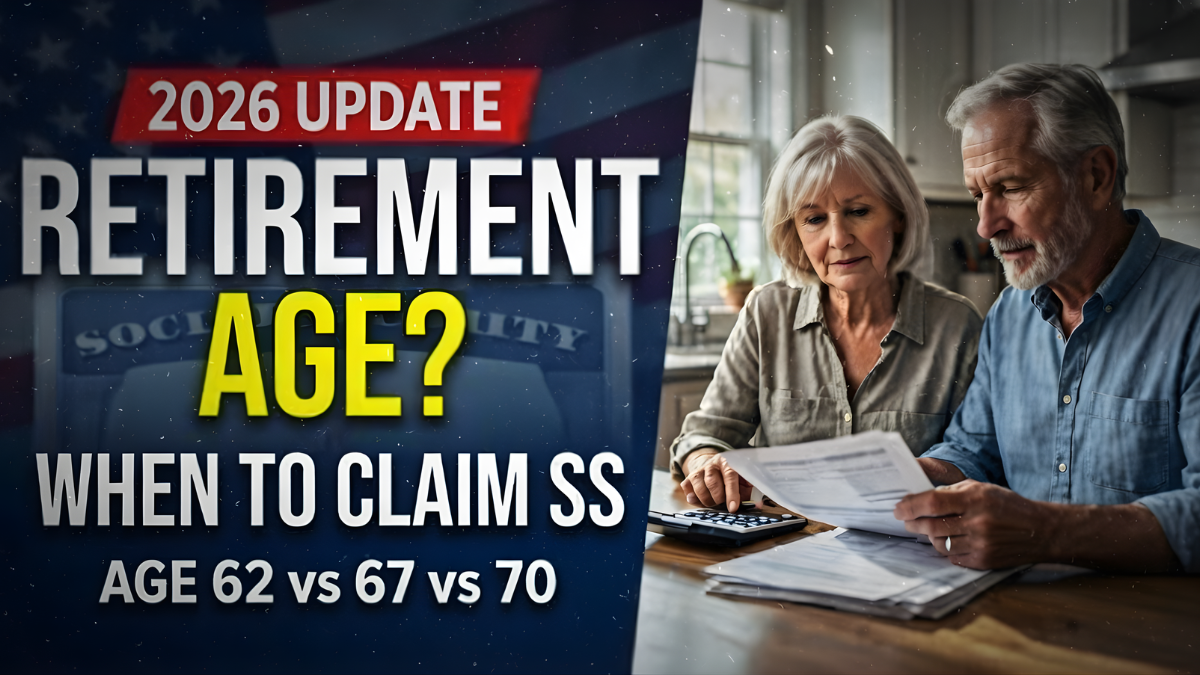

As 2026 approaches, Americans planning retirement are paying closer attention to one critical factor that can permanently affect their income. Your Social Security retirement age. With rising living costs, longer life expectancy, and ongoing discussions around benefit sustainability, many people are asking the same question. When is the best time to claim Social Security benefits in 2026?

Understanding the Social Security retirement age chart for 2026 is essential before making a decision that cannot be undone.

What the Social Security Retirement Age Means in 2026

Social Security retirement age refers to the age at which you can begin claiming retirement benefits and how much you will receive each month. While you can start benefits as early as age 62, doing so comes with permanent reductions. Waiting longer can significantly increase your monthly payment.

In 2026, the full retirement age depends on your year of birth, and many future retirees are discovering that full benefits now require more patience than in previous decades.

The system is administered by the Social Security Administration, and its rules apply nationwide.

Social Security Retirement Age Chart for 2026 Explained

For people reaching retirement eligibility in 2026, the retirement age structure remains consistent with recent years.

Individuals born in 1958 reach full retirement age at 66 years and 8 months. Those born in 1959 reach full retirement age at 66 years and 10 months. People born in 1960 or later must wait until age 67 to receive full benefits.

Claiming benefits at age 62 results in a permanent reduction of up to 30 percent depending on your full retirement age. On the other hand, delaying benefits beyond full retirement age increases payments through delayed retirement credits until age 70.

Claiming at 62 vs Full Retirement Age in 2026

Many Americans consider claiming benefits as soon as they become eligible at age 62, especially if they need income immediately. However, claiming early in 2026 can significantly reduce lifetime benefits.

If your full retirement age is 67 and you claim at 62, your monthly benefit could be reduced by roughly one third. That lower amount stays with you for life, even after reaching full retirement age.

Claiming at full retirement age allows you to receive 100 percent of your earned benefit, without early filing penalties.

Why Waiting Until 70 Can Pay Off

Delaying Social Security benefits beyond full retirement age increases monthly payments by about 8 percent per year until age 70. For individuals with good health and a longer life expectancy, waiting can dramatically increase lifetime income.

In 2026, those who delay benefits to age 70 may receive up to 24 to 32 percent more per month compared to claiming at full retirement age, depending on birth year.

This strategy is often beneficial for higher earners and individuals who expect to rely heavily on Social Security later in life.

How Work and Income Affect Claiming in 2026

If you claim Social Security before full retirement age and continue working, income limits apply. In 2026, exceeding the annual earnings limit can result in temporary benefit withholding.

Once you reach full retirement age, these income limits disappear, and benefits are recalculated to credit months when payments were withheld. Many early claimers misunderstand this rule and are surprised when payments stop temporarily.

Understanding how work income interacts with retirement benefits is crucial when deciding when to claim.

Health, Longevity, and Personal Circumstances Matter

There is no universal best age to claim Social Security. Health status, family longevity, marital situation, and financial needs all play a role.

Those with health concerns or shorter life expectancy may benefit from claiming earlier. Individuals in good health with family histories of longevity often gain more by waiting.

Married couples also need to consider spousal and survivor benefits, as claiming decisions can affect household income long after one spouse passes away.

Common Mistakes Retirees Make When Claiming

One of the biggest mistakes retirees make is claiming early without understanding the long-term impact. Others assume benefits will disappear if they wait, which is not true under current law.

Some retirees also overlook how inflation adjustments work, believing early claiming will be offset by future COLA increases. In reality, COLAs are applied to the reduced benefit amount if you claim early.

What Retirees Should Do Before Claiming in 2026

Before making a decision, retirees should review their Social Security statements, estimate future benefits at different ages, and consider other income sources such as pensions, savings, or part-time work.

Running multiple claiming scenarios can reveal large differences in lifetime income. For many people, waiting even one or two extra years can make a meaningful difference.

Conclusion

The Social Security retirement age chart for 2026 highlights how timing can significantly impact your financial future. While claiming early offers faster access to income, it comes with permanent reductions. Waiting until full retirement age or delaying to age 70 can increase monthly benefits and long-term security. The best time to claim depends on health, finances, and personal goals. Taking time to understand the rules before claiming in 2026 can help ensure you make the most of the benefits you earned.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice.